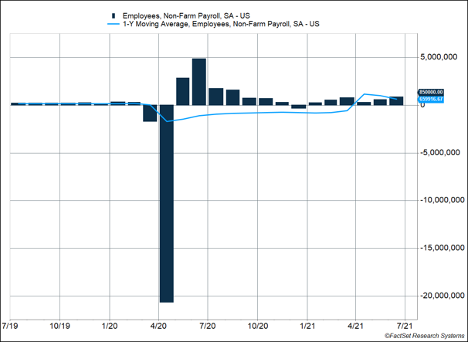

U.S. payrolls jumped 850,000 in June after two months of mediocre hiring (Figure 1). With these gains, the private sector has now reinstated 73% of the jobs lost during the pandemic. Restaurants and hotels led the hiring, as the leisure and hospitality industry added 343,000 new positions.

Key Points for the Week

- The S&P 500 climbed 8.5% in the second quarter and has now risen 16.7% over the last year.

- The U.S. economy added 850,000 jobs in June, beating expectations of 700,000.

- Average hourly earnings rose a moderate 0.3% last month.

Concerns about inflation dipped when average hourly earnings rose 0.3% last month. Wages are 3.6% higher than a year ago, which is only just above the 3-3.5% trend prior to the pandemic.

Stocks surged again last week and wrapped up a profitable quarter. The S&P 500 gained 1.7%. The MSCI ACWI gained 0.4%. The Bloomberg BarCap Aggregate Bond Index added 0.5%. The S&P 500 picked up 8.5% during the quarter and is now 16.7% higher, which includes gains made during the first days of the third quarter.

Fundamentals will take center stage in coming weeks as companies begin to report quarterly earnings. Earnings are expected to leap 63.6% from depressed figures during last year’s lockdowns.

Figure 1

Figure 2

Heading in the Right Direction

One experience Generation Z will miss out on is taking wrong turns on vacations en route to historical sites of questionable visitation value. Being able to read a map, plan ahead, and watch for road signs isn’t as crucial a skill as it once was. The map systems on our phones make it a lot easier to ensure we are heading in the right direction.

However, those map-reading skills have not lost all their usefulness. Predicting how the U.S. economy will recover requires abilities similar to navigating before smartphones. Based on last month’s job data, it looks like the economy is making up for lost time, after falling short the last couple months. June payrolls rose 850,000, surpassing expectations of 700,000. June’s gains were roughly equal to the gains in the previous two months combined (Figure 1).

The jobs returning to the economy were in locations one would expect: restaurants and hotels. More Americans are venturing out on vacations (hopefully with fully charged smartphones) and eating in restaurants. Even when seasonal hiring trends are eliminated, the leisure and hospitality industry still added 343,000 jobs. Those gains accounted for 40% of the overall increase. More states and cities reopening were big contributors to the gains.

The jobs market isn’t the only place the country is experiencing gains. The S&P 500 rose 8.5% in the second quarter, adding to solid gains from the first quarter. Counting the 0.5% increase early in the third quarter, the S&P 500 is 16.7% higher this year.

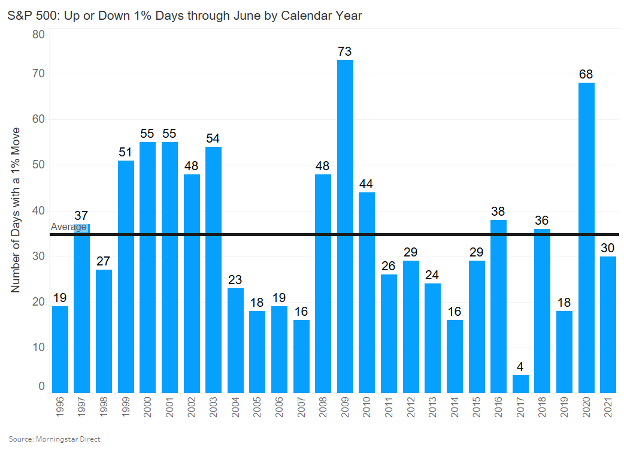

Like traveling, it seems like owning stocks used to be riskier. During the first half of the year, the S&P 500 moved more than 1% in either direction 30 times (Figure 2). Only 10 of the 30 moves were negative. While the S&P 500 dropped more than 30% during the initial stages of COVID-19, it has since rallied sharply and recorded several new highs. Sticking with the market through the pandemic challenges has paid off.

During the days when map reading was a useful skill, one risk was complacency. The longest unnecessary detours sometimes occurred because the navigator was a little too sure they were on the right route. Prior to COVID-19, the U.S. stock market had gone the longest period ever recorded without a decline of 20%. While the S&P 500 dropped more than 30% during the pandemic, it only closed 18 days more than 20% below its previous high.

As we recognize the benefits of technology, such as smartphone maps and vaccines that protect us, keep in mind these technological advances haven’t eliminated the normal risks that come from investing in the markets. Like it was among map readers of the past, complacency can be a bigger risk than you think.

—

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.factset.com/hubfs/

https://www.bls.gov/news.release/empsit.nr0.htm

https://fred.stlouisfed.org/series/CES0500000003

Compliance Case # 01075661